BLUF: I’ve found that overcoming difficult experiences can be a source of both short term and long term happiness. You can do this intentionally by choosing to attempt physically and mentally demanding challenges. Short term it can make normal life feel more extraordinary. Long term, it can build mental toughness and provide experiences that you can reflect on with gratitude and pride.

I participated in my 4th ultramarathon trail race recently. It was 32 miles in mountainous central New York with 7,200 feet of elevation gain over the race. That’s like climbing up a small mountain over the race and going up (and down) inclines that would rival the steepest black diamond downhill skiing trails at times. There were plenty of moments where my legs ached, my stomach hurt and I mentally doubted my desire to keep going on. But go on I did, and I finished my 3rd ultramarathon in around 8.5 hours.

The experience after finishing a race like that is in some ways as unique as the event itself. After something that long and grueling you feel disgustingly dirty from the dust, sweat, water and dirt along the way. You’ve burned close to 6,000 calories so your body feels depleted and is craving food. You’re so tired that aside from eating you just want to rest and sleep.

A funny thing happens for me, though, when you go through something that difficult. Every bite of food tastes that much more flavorful and satisfying. The shower I take post race feels so refreshing and rejuvenating that I often just sit there and let the water run over me. I can’t keep my eyes open and my body is craving the feeling of that soft, glorious bed. In other words, everything feels better and I feel happier.

Often people think about making life happier by seeking out an easier, pleasure filled path with less pain. In reflecting upon this post race I wondered – can doing intentionally hard or grueling things on purpose make us happier? Could there be a path to happiness by persevering through pain? That’s an idea we’ll explore today.

We all have a “base” level of happiness in our lives. The day to day happens in life and we feel some normal or average level of happiness. Studies have shown that for some reason this “base” level of happiness for people is usually around a 7 on a 1 to 10 scale. The hedonic treadmill or hedonic adaptation is the notion that after a positive or negative event things revert fairly quickly back to our base level of happiness. It’s great to adapt and revert to that baseline when something bad happens. Not so great when something good happens.

Here’s a real life example of this in action. You have a cute little starter home in a great neighborhood. Life is good and you’re happy at a base happiness of 7. But, you have big dreams. You always wanted a mansion in the hills and through hard work and luck you make it happen. Your happiness spikes to a 10 when you close on the house and move in.

A funny thing happens though. You get used to coming home to the dream home and each day you live in it it’s normalized. It’s just home to you now just as the starter home was previously. Happiness reverts to a 7 except the baseline 7 level of happiness is now living in a mansion.

You can see how this cycle can be problematic when you’re constantly chasing happiness and expecting that level 10 to stick. When you chase after nice things to make you happy it just raises the bar for what is normal in your life making it harder and harder for something to make you feel good. It’s one of the reasons that buying stuff is all just short term spikes of happiness that then stop feeling good.

However, I’ve found that the same phenomenon seems to work in my favor when I do hard thing.

Doing Hard Things: The Hedonic Treadmill in Reverse?

I’ve noticed that for me, the process of training for and completing something really hard is like making that hedonic treadmill work for me.

My everyday life might feel like that comfortable level 7 of happiness but when I’m attempting something really hard like an ultramarathon, it’s not a 7. When I’m 25+ miles into an ultra it gets pretty rough both physically and mentally.

My feet hurt. My body aches. My stomach is usually upset. I’m likely either overheating or cold depending on the race. I’m on the pain train and there’s no getting off of it unless you quit. Oh, and boy are there times when you want to quit. It’s a mental struggle at time to just put one foot in front of the other and keep going. That 7 level of happiness is long gone and I’m in the 3-4 range if not lower.

When I’m in the worst of things, the everyday life level of happiness seems like a far away dream. When I finish doing the hard thing, though, that happiness returns to 7 and then flips positive. Why? Well there are a number of reasons:

Everything feels better by comparison – When you’ve punished your body in a number of ways, everything by comparison feels good. Every bite of food that I put into my mouth tastes flavorful. Taking a shower after being disgusting for 8+ hours feels luxurious and rejuvenating.

Feeling of accomplishment – There’s really nothing quite like the feeling of overcoming something that is really hard or even something that you though was impossible for you. The sense of personal pride is amazing. It feel great to share your accomplishment with family and friends.

Long Term Positive Effects:

The short term positive effects of doing that hard thing are great. However, you can’t escape the hedonic treadmill and before long your body and mind will revert back to it’s baseline happiness level. Despite that, there are longer term positives to draw from that hard experience:

Memories of the Accomplishment – As I mentioned in Happiness Dividends, our experiences pay us back long after they’re over. Looking at that finishing medal and seeing social media reminders from that race in the future will all me to draw pride and happiness from that event for years to come.

Building Mental Toughness – You just overcame something really hard. How much easier does the hardest work day seem by comparison? When you do hard things, it’s building mental muscle that lets you handle life more easily in the future.

Another Cookie in the Cookie Jar – David Goggins has a concept in the book Can’t Hurt Me called the cookie jar. When you overcome something hard, you have that “win” captured in your mind like putting a cookie into a cookie jar for later. Later in life, when the shit gets tough, you can reach into your mind (cookie jar) and recall that past victory (cookie) and use it as mental motivation. It’s a great way to summon mental and physical strength in the present from past victories.

Find Your Hard Thing- Incorporating Hard Things Into Your Life

You may be thinking to yourself “that’s great, but I don’t want to run an ultramarathon.” Great, don’t do it! Hard is relative. Endurance sports is where I am now on my journey of hard things but you don’t have to start there. Hard to me is anything that mentally, physically or emotionally pushes you way outside your comfort zone.

Complete something that forces you to overcome a fear that you have: fear of failure, fear of public speaking, fear of flying, fear of heights, fear of small spaces.

Build up to running a 5k

High intensity short exercise – High Intensity Interval Training (HIIT) / CrossFit X days a week

Complete an endurance race of some kind.

Complete a 24 hour (or more) fast

Try Skydiving

Action Steps

Think about something hard that would put you outside of your comfort zone.

Make a plan and do the hard thing.

Make sure you hold yourself accountable to doing it. Sign up for a formal event if you can to ensure you have something concrete to work towards.

BLUF: Financial decisions aren’t just about math and logic because humans aren’t robots. The most rational decision isn’t necessarily the right one for you if you can’t handle it emotionally. Our money choices just need to be reasonable. They need to allow us to feel good about them, stay the course and sleep well at night.

What Should I Do?

There’s a question that causes internet debates, and sometimes arguments, almost daily in the personal finance space. The question is: “what should I do?” or “what would you do?” and then insert a financial situation here ________. The financial situation varies but a few common ones are:

Should I use extra money to pay down my mortgage faster or invest it?

I came into a large amount of cash, what should I do with it?

Should I use the debt snowball or the debt avalanche to pay off my debt?

There are typically two sides squaring off: the most financially optimal decision in the situation (what make or saves you the most money) versus some less financially optimal decision.

One group of people will be behind the financially optimal choice explaining the situation in terms of what the math “says”. Another group of people will offer up a choice that isn’t as financially optimal on paper but one that they’re very happy to have made and would make again. Which side is right? Which side is wrong? What should you do?

Rational vs. Reasonable

These two sides represent a conflict in financial decision making. Morgan Housel presented these two sides in one of my favorite books: “The Psychology of Money” as Rational vs. Reasonable. Rational being the most mathematically optimal decision and reasonable being a less optimal decision that is still financially sound and feels good. I found this to be the most impactful concept in the book and it’s what we’ll explore in depth here.

The Elephant And The Rider

Before we talk about rational vs. reasonable, I think it’s important address the elephant in the room (I know, I couldn’t resist). There is more to decision making than just unemotional logic and reason.

In the book Switch by the Health Brothers I was introduced to the concept of our thinking and feeling brains. There are two different decision making forces inside of us as complicated human beings: the thinking brain and the feeling brain.

The thinking brain is the logical, rational part of our brains. It’s the part running calculations and spreadsheet to determine how much house we can afford based on our budget, down payment, interest rate…etc. It’s the part of the brain at the grocery store buying the cheaper tuna fish based on unit price.

The feeling brain is emotional and is making decisions based on how we feel about the decision. It’s the part that walks into an open house for a home that you can’t afford and makes you say: “screw the budget, this feels like home.” It’s the part that sees that shiny black corvette on the car lot and now all you can think about is how awesome it will feel to drive that each day.

A wonderful metaphor for the power of these two decision making forces is an elephant with a human rider on top. The feeling brain is actually the massive, powerful elephant while the thinking brain is the puny rider on top.

That thinking brain rider may think that they’re in control because the elephant often listens to their commands. However, when the elephant doesn’t agree with the command the rider quickly learns who’s in control and they’re just along for the ride. The feeling brain elephant is in control and if there’s a conflict between the two it’s going to win. Every. Single. Time.

We like to think of financial decisions as something purely mathematical where logic can be applied to determine our decision. Being an engineer, I always assumed that all of my decisions were coming from a place of logic and reason in my brain. However, both thinking and feeling brains are involved and that feeling brain holds the power.

Rational vs. Reasonable vs. Emotional

I like to think about our financial decision making as a spectrum with pure math on one end and pure emotions on the other.

Rational – A decision that’s based on what the logic or math says. The financially optimal choice to make without taking feelings into account.

Emotional – A decision that’s based on what feels right. You don’t really know the financial implications (good or bad) of your choice because they haven’t been considered.

Reasonable – A financially sound decision that’s a compromise between what’s most optimum financially and what feels right based on a persons experiences, goals and risk tolerance.

I think it’s important to recognize that while the rational decision, the financially best one, could be the same for a range of people, the emotionally best decision is highly personal and will vary widely. The feeling part of our brains brings into our decisions all of the life experiences that we’ve had along the way to shape us.

A retired person that sold all their stocks at the bottom in 2009 and never recovered is going to feel very different about the stock market than a younger investor who rode the subsequent bull market. A person that went bankrupt and lost their home in 2009 will feel very differently about mortgages, debt, leverage and risk than someone that’s never been foreclosed on before.

Rational vs. Reasonable – Real World Examples

With that framework in mind, let’s talk about some commonly debated decisions that show both sides of rational vs. reasonable argument. For each I’ll show the commonly argued rational choice along with some perfectly reasonable choices. It’s important to keep in mind that just because you wouldn’t choose one of the reasonable choices below doesn’t mean that it isn’t reasonable for someone else.

You have no debt except for your mortgage and you have extra money at the end of each month. Should you invest that money for retirement or make extra principle only payments to your mortgage to pay it off faster?

Rational Choice Argument: If your mortgage interest rate is 2-5% (or less), then paying extra to your mortgage is going to build wealth slower than investing that money in an S&P500 index fund that averages 8% returns historically.

Reasonable ChoiceExamples:

Pay some extra to the mortgage and invest some of the extra.

Put all extra extra cash to the mortgage to pay it off as fast as possible.

Reducing your retirement contributions to let you pay off your mortgage faster.

It might be really important to someone to be debt free. I’ve heard people describe the feeling of paying off their mortgage as being one of the best feelings ever and that they wouldn’t trade it for the world.

Lump Sum Investing vs. Dollar Cost Averaging (DCA)

If you received a large chunk of money, should you invest the entire amount into the stock market at once (lump sum) or stretch out the investment of that money over weeks, months or years (dollar cost averaging (DCA)).

Rational Choice Argument: The S&P500 over time goes up on average, and you can’t time the market, so performance will be best if you put the whole lump in at once and give the money the maximum time in the market.

Reasonable Choice: Dollar cost average the money into the stock market. Come up with a schedule to invest that money over weeks, months or even years and put it on auto-invest.

The pain of losing money is far greater than the pleasure of increasing it. Studies have shown that the pain of losing $1,000 is twice as great as the pleasure of gaining the same $1,000. The goal here is to get the money invested as quickly as possible and keep it invested, but in a way that won’t make you do something irrational.

If you invest $100,000 as a lump sum, the market drops 10% and you sell and sit in cash for the next year then you aren’t going to come out ahead. I’d rather someone invest $10,000 a month for 10 months because they feel more comfortable doing than do a lump sum that will make them very nervous.

Debt Avalanche vs. Debt Snowball for Debt Payoff

The debt avalanche payoff method means that you pay off debts in order of the highest interest to the lowest. The debt snowball method means that you pay off the debts in order from the smallest balance to the largest, regardless of interest rates on the debts.

Rational Choice Argument: The avalanche method will get your debt paid off while paying the lowest amount of interest possible.

Reasonable Choice: Using the snowball method or some combination of the two methods to ensure that you get some quick wins and stick with the process.

Paying off debt can be analogous to trying to losing weight on a diet. If you choose a method where it’s hard to see some progress right away it’s discouraging and you may give up altogether. For example, if the first debt you tackle is a large one that takes a year to pay off by the avalanche method then you might just quit. If the first debt is a small $500 debt on a 0% interest offer but you get to eliminate that bill in one month then it’s reasonable to go for the easy victory. That feels good and can re-energize you to keep going.

All of this is well and good, but knowing that we’re each uniquely messy emotional beings, how do we make the most reasonable choice for us? Here is my suggestion for working through a decision:

Make a list of your big goals that relate to the decision at hand – It can be easy to get into the details of a situation and forget about the larger picture. If your big goal is to retire early, sell your house and travel the world then that will heavily influence the decision to pay down your mortgage versus invest.

Really understand the arguments for the mathematically “optimal” approach – Even if you don’t take the perfectly rational option, I think it’s key to fully understand what that choice would be and why. Why does the math show that lump sum investing will outperform DCA historically? Through that education it might actually change your feelings about the risk at play and what the most reasonable choice is for you. You could also run some “what if” scenarios.

For example, if you’re unsure about lump sum versus DCA, simulate what would have happened in a scenario. For example, if you lump sum invested $150,000 into the S&P500 in January of 2019 how would the performance today compare to investing $50,000 on 1/1/2019, 1/1/2020 and 1/1/2021?

Write down any fears or worries that you have about the decision – It’s important to self reflect and understand that there are emotions at play with financial decisions. If there are certain outcomes that you’re afraid of happening then you need to acknowledge that. By identifying and acknowledging that worry you can then come up with options to address that fear.

As a simple example, if one spouse is the breadwinner and the other takes care of the household then the household maintainer might be worried about what happens if the breadwinner dies. This risk and concern can be mitigated with term life insurance.

Consider options that aren’t just “all or nothing” – Sometimes people get paralyzed because they only think in terms of decision extremes. In the pay down your mortgage example, I either pay nothing extra to the mortgage or I aggressively put everything extra to the mortgage. Life isn’t about binary decision making (2 choices). If you really aren’t sure what to do choose an option that does both. Take 50% of extra pay and put it toward the mortgage principle and invest the other 50%. One way to get ideas is to ask other people what they would do in your situation. Just be careful to use the responses as ideas, not to make the decision for you.

Make a decision but don’t be afraid to revisit it – Many financial decisions can be reversed or adjusted if you don’t feel good about your decision. Don’t be paralyzed by a decision that can be easily adjusted in the future if it doesn’t work out as planned. Make a decision but then check back in periodically to see how you feel about it. If you have anxiety and check a new investment daily perhaps you’ve taken on too much risk and you need to change course.

Key Takeaways

Financial decisions aren’t just about math and logic because humans aren’t robots. The most rational decision isn’t necessarily the right one for you if you can’t handle it emotionally. Our money choices just need to be reasonable. They need to allow us to feel good about them, stay the course and sleep well at night.

There are a wide range of reasonable choices out there so be careful about giving or receiving one size fits all advice. What’s reasonable for one person based on their experiences, goals and risk tolerance might be completely unreasonable for another person.

Nobody can tell you what’s the most reasonable decision for you, except you. Keep that in mind when asking others what they would do in your situation. A good fixed fee financial planner might be the most skilled at doing this for other people as they are trained to understand your goals, risk tolerance and worries and then offer up options that they think align with that information.

It’s okay to choose reasonable over rational. Don’t let others get you down because your rational choice didn’t maximize your wealth. Financial metrics aren’t the only indicators of a good decision.

BLUF: Budgeting is financial planning at the monthly level. It lets you manage your way through the variability of life while staying on track to hit your long term goals. Don’t let it control your life though. Your plan needs to adapt to life, not the other way around.

Just don’t budget and you don’t have to worry about your spending. End of article! Just kidding, that doesn’t work. A plan to ignore reality only works in the short term before reality comes back to smack you upside the head. Reality can hit pretty hard, too.

I resisted budgeting for a long time. Each year I did a little bit of work at the end the year to summarize my annual spending in Excel. I tried expense tracking in Excel for 3 months since I knew it well and it was painful. Even for me, a lover of spreadsheets. When I found the You Need A Budget (YNAB) product it was a 2 for 1 deal that did both expense tracking and budgeting. I’m the type of person to go all in and give something a try. So I did!

This article is going to cover how I zero based budgeting with YNAB, the benefits that I’ve discovered since I started budgeting and some tips for you as you embark (or continue) on your own budgeting journey.

A budget in its most basic form is a financial plan over a period of time but most commonly a year in personal finance. This financial plan includes how much we plan to earn, spend and save. Having a plan gives you the day to day flexibility to live life while month to month you have a north star helping to keep you on track to your overall goals.

Budgeting is the process of creating and executing that financial plan. It’s figuring out in advance of money arriving how you plan to save and spend that income. If you’re reading this blog you might very well have some larger financial plans for how you’ll get out of debt, reach FI or just save X amount this year. Budgeting is financial planning but on a smaller scale since it has monthly and annual time horizons.

Zero Based Budgeting

Zero based budgeting is creating a plan for every dollar that comes in via your paycheck or whatever income source you have. It may sound intimidating but with a tool like YNAB it’s much easier. You plan for how those dollars will be assigned for savings, spending that month and larger expenses that will happen in future months. Don’t worry, this will make more sense when I get into some examples.

Tracking Spending vs Budgeting

Sometimes people talk about tracking spending and budgeting as if they are the same thing. They are NOT!

Tracking Spending – You spend money without any awareness of how much you could spend. You record the transactions and categorize them after the spending is done.

Budgeting – You have a plan for how your income will be spent before you actually spend the money. As life happens and money is spent you tweak your budget as needed on a month to month basis to try and keep the overall spending for the year to your plan.

One of my goals with this article is show how you can make budgeting work for you and encourage people to give it shot. Before I get into the specifics of how I work a budget on a monthly basis I’m going to go over what you need before you get started yourself.

All of the pieces of information below feed the basic formula of income = savings + expenses. You don’t need to know exact numbers for each area but you do need at least an educated guess.

Calculate Your Annual Income

You need to know roughly how much money you make in a year so that you can make a plan for have much you can realistically save and spend. If you’re a salaried employee that gets paid every 2 weeks then you get 26 paychecks a year. If you get paid $3,000 a paycheck then that’s $3,000 * 26 = $78,000 take home pay a year.

Measure or Estimate Your Annual Expenses

Here is where tracking your expenses or at least doing an annual spending summaries comes into play. You need to know roughly what your expenses are for a year. Not only that, but for each budget area where spending is variable like groceries or entertainment you need to make a guess at what you want to spend per year.

That’s why it’s critical to have expense tracking down first to feed into your budget plan. More details in how to do that in the tracking spending article. In my case my 2021 spending target was $52,000. If you have no idea just get 3 months of data and use that to forecast what a year might look like.

The 3 month look with give you the common expenses but make sure you capture all the annual and semi-annual expenses. It’s these infrequent expenses that usuaully surprise people and throw off their spending if they aren’t planned. Taxes (property, school, income), insurance premiums (car, life, umbrella) just to name a few.

Come Up With An Annual Savings Target

Why come up with an annual savings target? It’s far too easy to just spend what you want and try to save the leftovers. I’m a big proponent of the “pay yourself first” approach to saving. Figure out what you can save each month and then setup a system where savings is required to be “paid” just like a bill.

In the image below you’ll see that I even arranged by category groups so that savings comes first. That’s not by accident, it’s to reflect my priorities. When I allocate monthly I go top to bottom and the savings accounts get “paid” first before I move to my core expenses.

Using the example so far, we’re taking home $78,000 in income and have expenses of $52,000. That leaves $26,000 ($78k-$52k) that could be used for savings.

Setting Up Your Budget Plan

I’ll warn you now, getting a budget setup the first time takes some work. It’s the hard part but once you’ve done it the work and time required month to month and year to year is very little.

Defining Budget Categories

This is already done! When you started tracking your spending you defined the buckets that you would use to track that spending. All we do now is use those same exact categories to use for our budget and plan for the spending that will happen in those categories.

Breaking Down Expenses & Saving Monthly

Most budgeting is handled monthly so the first task to project how much you need to plan for each month in that budget category.

The Extra Paycheck “Problem”

The first topic to touch on though isn’t really a problem, but can cause headaches. It’s the fact that budgeting is monthly but paychecks are usually every 1 or 2 weeks. Because of that the frequency of your pay isn’t consistent each month.

In our example of getting paid $3,000 every 2 weeks you will technically take home $78,000 a year. Divided into 12 months that’s $6,500/mo on average. Life isn’t average though. Cash flow wise you’re going to get $6,000/mo for 10 of those months (2 paychecks) and the other 2 months you’ll get $9,000/mo (3 paychecks).

To avoid having a problem on a monthly basis I simply make sure that the targets that I set for my budget monthly fit into the $6,000/mo guaranteed income. When those extra paychecks come they go towards larger annual bills or additional savings.

Breaking Down Expenses

I’m a big spreadsheet guy so I used that to figure out my 2021 budget. Using my expenses from 2020 as a guide for what was reasonable I came up with a yearly target for each category and then let the spreadsheet calculate the monthly equivalent. If you want to make the numbers easier make sure your yearly expense values are easily divisible by 12 or you’ll end up with odd monthly values. Ex. Round $1150/yr to $1200/yr so that it’s $100/mo instead of $95.833333333333333333333333333333333333.

It’s important to do this with ALL expenses. One place where people often mess up with their budget is to not include annual expenses because they aren’t a consistent bill. My taxes, for example, are $5,600 a year but are

Breaking Down Savings

You rinse and repeat the same process with savings goals which should be easier because there are usually few buckets to deal with. For example, if you want to max out your IRA for the year that’s $6,000 or $500/mo.

Setting Your Plan On Autopilot with YNAB

You now know how much you need to save and spend monthly in each category to stick to your budget. Time to put those details into YNAB so that each month you don’t need to remember what your goals are supposed to be.

Setting Spending Targets

Things like groceries are expenses that happen each month but the exact amount spent is going to vary. YNAB lets you input a target spending amount and will remind me to save $500 each month for groceries and other household consumables (toilet paper, paper towels, shampoo). If you allocate $500 to groceries and only spend $450 that month, YNAB will roll over the extra $50 to the next months grocery budget. You can either budget another $500 to build some buffer or only budget $450 more instead of the usual $500.

Sinking Funds / Monthly Savings Targets

If you have infrequent expenses like auto repairs you need to plan for those as well. A sinking fund is a temporary savings bucket to be used for expected future spending like car maintenance. It won’t happen every month, but you’ll need the money at some point. I plan for $600/yr so that’s $50/mo.

YNAB has a savings target option which expects you to save a target amount each month. This is what you’ll use for both sinking funds and savings goals.

Saving For Big Bills / Goals

Budgeting for big, long term expenses and goals can be the most challenging. YNAB makes this easy by letting you set a dollar amount and a date that you need the money. Then, it calculates how much you need to budget that month to stay on track towards that savings goals.

For example, my property taxes are once a year in February and are a big bill. YNAB has calculated that I need $309.72/mo from now until then to hit that goal. If an unexpected bill came up and I couldn’t save for this one month it would automatically recalculate the new monthly amount for me.

Monthly Budgeting In Action with YNAB

Having a plan is great, but life happens and nothing goes to plan. Life is messy and your spending will never align exactly to your plan. I think this is a point of frustration that causes some to give up on budgeting. Hang in there! To me this is where having a good tool like YNAB can let you roll with the punches and stay on track. Did you see what I did there? 😉

Overview

Zero based budgeting means that when you get paid it’s time to give those dollars a job. In the example below we were paid $3,000 and those dollars need to be assigned for our planned expenses in September. “Planned Spending”, also called Assigned, is how much you want to budget towards each category for that month. Actual spending tracks the real spending that occurred.

As I assign dollars it subtracts them from the “ready to assign” bucket automatically. If categories have funding goals then as I hit that goal YNAB will tell met that I’ve fully funded that category for the month.

An example of rolling with the punches. Usually I budget $250/mo for fun and entertainment. In June I had a big healthcare bill ($654) that was unexpected. As a result I only budgeted $50 to fun and entertainment that month as I needed the $200 to cover my healthcare.

Because I had been saving $250/mo previously in my fun budget and not using it I had a lot in the fun sinking fund. I spent $691 for fun in June, only allocated $50 in new budget money to the pot and still had $796.62 available to spend. That’s the power of sinking funds, planning ahead (budgeting) and having software like YNAB to let you adjust on the fly.

Other budgeting methods

There are a LOT of budgeting options out there that are well covered in other articles so I’ll let you explore those on your own if you don’t like zero based budgeting. One of our favorite finance shows forces people to use cash in jars to manage their money. That’s also zero based budgeting but in a very rudimentary way. YNAB is essentially a fancy digital jar system that works across all bank accounts and credit cards.

https://youtu.be/S3ivBN1o2TY?t=579

Benefits of Budgeting:

There are some benefits of budgeting that I’ve noticed along the way that I wanted to share.

Stress Reduction

Having a budget with all these little sinking funds for infrequent expenses reduces the worry that I’m not going to have the money if something pops up. These little sinking fund buffers also make it easier to cover one area that might blow up unexpectedly in a month without having to go into debt or my emergency fund. I just shift spending from one area to another.

Satisfaction of Hitting Little Goals

There’s some odd satisfaction that I get from assigning money to each category every month and seeing YNAB tell me that I’m “Funded” or “On Track” with my plan. It reinforces to me that I have a plan and I can check the box because I hit the plan for that month.

No Guilt About Spending Money

One area where frugal people sometimes struggle is that they have guilt about spending money. I think budgeting helps with that guilt in that once the money is in the budget it’s a part of my plan to spend it. In July I spent $1,045 on Elton John and Tom Segura tickets. It fit into my budget so even though they’re the most expensive tickets I’ve ever purchased I didn’t feel guilty one bit. Okay, the $700 in cash back rewards that I used helped too.

Less Worry About Stolen Accounts

With YNAB I see all the spending, real time. I don’t worry about a card being stolen because I’ll see a fraudulent charge as soon as YNAB imports it. I no longer have to look at credit card statements to make sure everything looks right a month after I spend the money.

Advice When Budgeting

Don’t choose an overly aggressive budget to start. Choose something that you know you can work within without deprivation. Worst thing you can do is get frustrated and quit because you can’t make the numbers work. For example, my spending budget is $52,000 for the year but I have an extra $3k of unplanned income in case something comes up. I think leaving a buffer of 5-10% of your annual budget as unassigned money helps you psychologically to deal with surprises. If no surprise expenses happen then you just have extra savings.

Life is unpredictable, expect your budget to flex and change. Have a plan to start but don’t be afraid to adjust that spending plan as the year goes on. Maybe you’ve found a way to save on your food budget and can lower that target. Maybe you’ve picked up a new great hobby that you love but costs $100/mo. DO IT, just make it work with your budget. Whatever you do, don’t be a slave to your budget.

Don’t worry about chasing perfection. If something doesn’t quite balance perfectly or some expense is unaccounted for don’t let it worry you. If it’s a small dollar amount that’s in the noise, leave it in the noise and don’t worry about it. It isn’t worth your time to chase perfection.

Don’t budget for the extra paychecksmonth to month. I covered this earlier, but if you get paid 2x a month most of the time don’t plan on those extra paychecks into your normal monthly plan.

Estimate your annual expenses, income and savings goals and then break that down into monthly amounts.

Use a program like YNAB to create budget categories and assign amounts that you’ll be targeting. Build slack into your budget, especially if you haven’t done this before.

Start tracking to your budget! Don’t be hard on yourself if you were way off with some estimates and have to change your plan. Your plan needs to adapt to your life, not the other way around.

BLUF: Having one years worth of expenses in accessible money can change your life. It can reduce financial stress, increase your confidence at work and provide the courage to take entrepreneurial risks.

There’s a magical thing that’s happened to myself and Mrs. MFI over the past 18 or so months. Over that period of time we’ve learned about the concept of FU money, implemented all pieces of the formula and have been able to feel the impact that it’s had on our lives. It’s had a really positive impact on our lives so I’m excited to share the formula for FU money that’s allowed us to reduce our life stress, manage uncertainty better and increase our confidence at work.

If you’ve been around the FI community you’ve probably heard about this idea but I think there’s a little more to the story than just saving a chunk of money. My goal is help you understand the formula that worked for us and give you the tools so that you can let FU money transform your world like it did ours.

Oh, side note. Hopefully it’s obvious that FU stands for f*ck you. If that bothers you and you want a family friendly version call it Freedom Unrestricted money. There’s going to be some swearing along the way via a fun video with J.L. Collins so skip that if it bothers you. Consider yourself warned!

The basic premise of FU money is very simple. FU money is having enough money to be able to get fired from your job or quit your job and be able to cover your normal life expenses until you find another gig. The “FU” part coming from the theoretical situation where your job or boss asks something of you that crosses a line. You financially could say “FU” and quit. You could also apply it in a situation where you don’t have an issue with your job but you want to give some kind of entrepreneurial activity a shot.

I will put my manager hat on and add the disclaimer that I don’t recommend telling someone FU when you quit or quitting in a disrespectful way in general. Ever. It might feel good in the moment but it’s almost impossible to repair a burned bridge when you leave a place on bad terms.

Depending on your location or industry if you burn a bridge it could have unintended consequences for many years or for life. You never know how word will get around if you go out in a blaze of glory causing it become difficult or impossible for you to get hired again. Your old company could put you on their do not hire list. Your old manager or management chain could change companies and recommend you not be hired if you applied to their new company.

The FU Money Formula

Having a heading that says “money formula” implies that there’s some math headed your way! Well, actually there’s almost no math but the formula part has more to do with the fact that to feel the impacts of FU money requires a few conditions to be met.

Knowing How Much You Need

How much money do you need to have FU money? Well, it depends. If you’ve used this article to calculate your emergency fund based on a job loss then you know how much money you need to survive until you find another job. If you want to plan for a worst case situation of quitting and therefore getting no unemployment benefits then leave out unemployment.

You need to know how much your life costs in order to know what it costs to cover that life without income. If that sounds like too much work then an easy rule of thumb is to have at least 1 year of living expenses in accessible money and you’ve got FU money. You understand what a year of expenses costs by tracking your spending.

Location, Location, Location

Here’s a key part of FU money that I didn’t get right until much later in life. You MUST have that FU money in a place that’s accessible now, not in retirement. It feels so obvious to write that I almost feel stupid doing so, but I didn’t experience any of the benefits described in the next section until the money was accessible. Not in a 401k, 403b, TSP or other account that’s harder to access until 59.5 years old.

Where should you put the money? Well, much like most of my emergency fund I keep my FU money in a brokerage account largely invested in stock index funds. It lets my money stay invested and continue to grow more aggressively. Sure, there’s the possibility of a market crash when I want to use my FU money but I look at both of these events as tail events. What’s less probable than one tail event? Two tail events overlapping in time.

You’re welcome to put your FU money other safer places like a bank account, high yield savings account (HYSA), CD or money market fund. A Roth account is also acceptable although I prefer to not touch that and let that money grow tax free. After all, you can’t just replace Roth contributions that you withdraw.

In Summary:

You generally need at least 1 years worth of living expenses in an accessible location to have FU money and start to feel it’s true benefits.

The Unexpected Benefits of FU Money

I didn’t intentionally go after accumulating FU money, it just sort of happened by accident. We starting tracking our expenses with YNAB and ran our emergency fund scenarios to know how much we needed to cope with a job loss. We then started investing in a brokerage and Roth account to have more accessible cash for the potential of early retirement.

When all those things came together and we realized that we had FU money, there were a number of other psychological benefits that we started to feel that impacted our lives in very unexpected ways. I talked with Mrs. MFI and she echoed feeling the same benefits that I’ll go through below.

As humans I think we naturally have fears of the unknown. The unknown normally associated with losing a job is how will you pay for everyday life and how long will you be without a paycheck? Not understanding how long you could survive without your job would be stressful for anymore.

Having FU money removes the fear of the unknown. You’ve run the math, you know exactly what would happen under various scenarios and you have the money to take care of your needs.

With FU money, you can sit back and confidently know “We’ll be okay”.

There’s something about knowing that you have your basic needs of life covered no matter what happens with your job that makes life and job stress just melt away. Life is uncertain and sometimes what happens with your job is out of your control. But FU money is something that you can control.

On the Job Confidence and Honesty

If you’ve ever watched office, then you know the classic scene where Peter interviews with “The Bobs.” I’ve included the clip below because it’s awesome and worth a watch even if you’ve seen it many times before.

https://youtu.be/j_1lIFRdnhA

What is different about Peter from the normal W2 worker? He has no fear about losing his job at this point in the movie. In the movie it’s because he’s hypnotized to not care and worry about his job. However, in the real world Mrs. MFI and I have found that having FU money has provided some of the same benefits.

Mrs. MFI has begun to stand up for herself when crappy co-workers treated her poorly and made for a poor working environment. FU money decreased her fear and worry about being trapped in a poor situation where she couldn’t say anything for fear of losing her job.

In my job FU money has provided me with the confidence to speak up when I see things that aren’t right but other are too scared to talk about. Even in the most ethical work situations there are plenty of people afraid to help point out a mistake to a superior out of fear. I’ll speak up with tact but that fear factor is gone for me.

I also began making decisions to fix things that were in the best interest of the company but were gray areas policy wise. Instead of asking for permission for anything uncertain I just made the decision.

FU Money: The Courage Creator

Did your grandfather take risks? I guarantee he did it from a position of f*ck you.”

J.L. Collins recreating “The Gambler”

To take a major financial risk like leaving a steady job to pursue starting a business is a scary idea. A steady paycheck is a safety net and you leave that behind for an unknown period of time to start a new business where income may be zero or inconsistent for some period of time.

FU money eliminates the risk of not being able to pay for life expenses while you don’t have income in the pursuit of a passion. In that way, FU money can provide the courage to pursue a venture that you really want to do but has risk associated with it. It could be the difference between living the life that you want and living a life of regret for not giving your idea a shot.

Start saving FU money! The key is that it’s NOT locked inside a retirement account like a 401k/403b/TSP. This could just be an extension on your emergency fund that’s stored somewhere that it will provide you growth and interest. For us, that’s both a brokerage account and a Roth account on top of some normal high yield savings accounts. Most of our FU money is invested.

Celebrate reaching it and small milestones along the way! Knowing that you have 3 or 6 months of expenses is empowering too.

BLUF: A key foundational skill is knowing how to track your spending. Tracking spending brings awareness to where the money goes so you can cut out the waste. Understanding your annual spending is also necessary to know how much money you need in retirement.

Mrs. MFI and I used to watch a online personal finance show called Til Debt Do Us Part. A guilty pleasure that both helped scare us into being good with our money and also made us feel good that we weren’t in financial situations like these. It was about couples who were in serious debt usually through excessive spending on stuff. The format of the show always includes the participants estimating their monthly spending and current debt levels and then the host reveals what they’re really spending using their statements. Watch until the 7 minute mark and you’ll see an example of that part of the show.

One common theme across every episode of the show is that the participants don’t track their spending and have no idea how much they’re truly spending. This couple had no idea what their monthly spending was and they also under estimated their total debt by $33k!

Television shows like this obviously use the most extreme cases for shock and awe entertainment value but unfortunately this is a pretty common problem. A Mint.com survey in 2020 showed that 65% of people surveyed didn’t know how much they spent last month.

What is Tracking Spending?

The concept of tracking spending is not hard to understand as the name mostly gives it away. You keep track of every dollar that you spend so that you can see where the money goes. A common way would be to record each financial transaction and categorize that transaction.

An example of tracking transactions is shown below from a tool called You Need A Budget (YNAB) which I love and use daily. Each line is a transaction that is then assigned a category. The categories can be whatever you want them to be. They’re just buckets to let you track the different types of spending. This becomes important later when you want to see at a lower level where most of your money is going.

There are many tools available to help with tracking and multiple ways to track spending which we’ll dive into later.

Tracking Spending vs Budgeting

I think it’s an important time to point out that sometimes people talk about tracking spending and budgeting as if they are the same thing. They are NOT!

Tracking Spending – You spend money without any awareness of how much you could spend. You record the transactions and categorize them after the spending is done.

Budgeting – You have a plan for how your income will be spent before you actually spend the money. As life happens and money is spent you tweak your budget as needed on a month to month basis to try and keep the overall spending for the year to your plan. A deep dive into budgeting here.

Why is Tracking Spending Important?

There’s a reason that I called tracking spending a foundational skill in personal finance. It is so critically important that you understand where your money goes and unless you track it you really can’t know for sure. According to this Mint.com survey, 65% of Americans had no idea what they spent last month.

People are also really bad at estimating since we’re filled with biases and optimism when it comes to our own actions. We never think we’re spending as much as we do so it’s critical to let the numbers do the talking. Otherwise we’re just guessing.

“What Gets Measured Gets Improved” – Peter Drucker

Peter Drucker said that famous quote many years. In business he was referring to the fact that if you track or measure something in business then you create awareness and you will improve what is being tracked.

Have you ever heard of a business that bought whatever it needed without tracking where the money was being spent on? Of course not unless it was an unsuccessful business. Why would you expect your household to be successful unless you track and understand where you are spending your money? When you track your person spending you create awareness of where the money is going and that will naturally lead to improvement.

At the end of 2018 I did my first annual summary of my spending for the year 2018. I didn’t track anything along the way but it was the first time even trying to see my overall spending and trying to categorize it. In 2019 I did the annual summary and bucketizing after the fact again but wasn’t yet looking for opportunities to reduce the spending significantly. It just seemed too painful to track every transaction.

In early 2020 I found FI and using 2019 data I started to making changes to reduce our spending. In December 2020 I went all in with YNAB tracking all expenses and truly budgeting for the first time. The results below speak for themselves. You can see what awareness of spending from tracking coupled with action can do for reducing your expenses. If you’re interested in the details of how I chopped down spending you can read about it here.

Beware of falling annual spending! 2019 included a $15,000 vacation instead of the normal $5,000 or the spending would have dropped every year.I guess the pandemic in 2020 made us eat more?I had an Amazon problem that I didn’t realize until I saw the data.

A simple formula for personal finance is savings = income – expenses. Most people they can’t make an instant change today and impact their income in a meaningful way tomorrow. As much as we’d love to give ourselves a raise when needed that’s rarely in our control. What we spend, however, is something that is in our control.

Tracking spending allows us to look at the areas where we might be wasting money and see what can be done to save money in those areas. Housing, transportation and food are the “big 3” expense categories for most people but all areas should be explored. Even saving $20 a week is still $1,000 a year.

FI Number Requires Annual Spending

This wouldn’t be an FI blog post without talking about the magic FI number which is based off 25 times your annual expenses (the 4% rule of thumb). What’s the only variable in that magical equation? Annual expenses? What does tracking spending tell you? Your annual expenses today.

Now, a true FI number is 25 * annual retirement expenses but until you get closer to FI enough to understand those retirement details you use your current annual expenses as your northern star.

The other magical thing to think about is your FI number in reverse. What do I mean by that? Since your annual expenses sets your FI number, ever dollar you reduce in annual spending saves $25 that you need in investible accounts. Every $1,000 in annual spending saved reduces your FI number by $25,000! How easy might it be to cut $20 a week in spending versus how hard is it to save $25,000?

For example, if my in 2018 cost $81,000. If that was my consistent spending then my FI number would be $81,000 * 25 = $2,025,000! Two million! My projected annual expenses for 2021 will be $52,000. Carried forward our FI number has dropped to $52,000*25 = $1,300,000. Wow. Making a number of life changes has dropped the amount we need to save by $725,000. That’s a lot of years of work time saved.

Laying the Budgeting Foundation

As previously mentioned, tracking expenses is not budgeting. However, it’s pretty hard to come up with a reasonable starting point for a budget unless you have general idea of how much money flows out of your wallet on average each month. Is $5,000 total a month reasonable? Is $500 a month reasonable to spend on food? $1,000? Your guess is as good as mine since everyone is different. Track spending first, then move onto budgeting.

How to Track Spending

Alright, enough already about why you probably should be tracking your spending and onto the real meat of the discussion. How do you actually track your spending?

Well, there are a variety of ways to track spending and you can choose the one that fits the amount of effort you want to spend, the level of detail you want and your personal lifestyle. I’ll go through a few common ones that I’ve used personally or have heard about others using.

For each method there are a variety of tools at your disposal to make the job easier. The good news? It’s never been easier to track your spending with so many great software tools that connect automatically with banks and credit cards.

Track At the Summary Level (Monthly / Yearly)

This is the “keep it simple” method to start. The goal here is to baby step you into the tracking spending without overwhelming you. After all, if you quit because it’s too much work then that’s not very helpful. If you’ve never tracked your spending before I’d recommend that you start here.

All we’re going to do is understand how much money you’ve spent on a monthly and yearly level using summaries from each account. You won’t necessarily understand how you’re spending the money yet, just how much. However, the hope here is that it’s easy and eye opening enough to make you want to dig for more answers.

Make a list of all the ways that you spend money – Checking accounts and credit card that you use.

Use online summary tools for each account to note how much you spent using that account or card last month.

Add up the spending for each account. For bank accounts be careful to ignore transactions where money was just moved from one account to another. You may want to use a spreadsheet to keep track of the spending for each account for that month. After all, you’re going to keep doing this, right?

Look at the data and see what it tells you. Are you spending more than you make? If you multiply that monthly amount by 12 how much would you spend a year? Unfortunately a single month will be a distorted view since everyone’s expenses has peaks and valleys.

Continue this to see what you’ve spent for the last 6 months. That’s generally a much better way to get a monthly average.

Jump back and pull the summary data from the previous full year and see what you spent last year. Credit cards often have online spending reports that can be pulled like the one from Citibank. The categories aren’t always the most useful but again the focus is the overall number. Does your annual spending surprise you compared with your annual take home pay?

Note: If your income is heavily cash based like a waitress or bartender and you don’t deposit that money directly into a bank account then it might be tricky to understand your spending in hindsight. If you don’t want to deposit the money then you’ll need to record each day how much cash income you’re making. That way you can check at month end how much cash you still have remaining on hand to determine what you’ve spent.

Track Every Transaction (What I use)

This is the most detailed method but with the tools available today it’s very easy to track and categorize each expense. It might take half a day or day to learn the tool and get it setup but after that it’s easy. As previously mentioned, I use YNAB and I probably spend 15 minutes a week dealing with transactions and categorizing them.

Choosing Categories

Using this method you’re going to keep track of every spending transaction and you’re going to put each transaction into a category or spending “bucket”. That way, you can measure each bucket at the end of every month or year and know what you’ve spent.

You have the flexibility to make as many or as few categories as you want. Just know that if you’ll have fewer categories you’ll have less granularity for your data in understand where the money is really going. For example, you could have the following categories as a very basic system:

Housing (Mortgage, Rent, Maintenance costs, related insurance)

Food (Groceries, eating out, alcohol, work lunches)

Everything else (Vacation, shopping, charity, personal care, entertainment, etc)

You could choose these 4 very high level categories of housing, transportation, food and everything else. It’s certainly better than nothing but it might not give you all the insights you want.

As you can see by the categories in parenthesis you can certainly break these high level categories down into many more categories. The key here is to just pick some categories and start tracking. There’s no perfect compliment and over time you’ll change what’s important for you to track.

What Categories I Use:

I use three high level groups for my categories called Core, Discretionary and Business expenses. Core expenses are everything I have to pay each month. If I lost my job I wouldn’t look at the core expenses for places to cut cost. That’s not to say that I couldn’t find something to cut, but I don’t plan financially on being able to cut here.

Discretionary expenses are the extra things in my life that I could partially or completely cut if I lost my job or something else bad happened. Now, this is a very individual choice for what goes in core versus discretionary. Don’t judge me for having charity in my discretionary expenses.

This is very easy because I don’t have to do anything usually with YNAB. All of my accounts are in YNAB and linked to my financial institutions. Whenever there’s a new transaction to do something with a dot will appear next to the account name and those transactions are imported. The software makes a pretty good guess at the categories most of the time but if it doesn’t know it says “This needs a category”.

Bob Johnson Toyota in this case was getting my car serviced so I selected the Auto Maintenance category in my Core Expenses.

Seeing Where the Money Went

By tracking spending at the transaction level it becomes very clear to see month to month and year to date exactly where your money is going. For example here is my June spending on Core Expenses.

We adopted a dog in June and with all the accompanying medical care and “stuff” that comes with a new pooch that was a high spending month. Same with healthcare as I had a procedure and accompanying appointments. If we took these two areas and multiplied by 12 months we’d get $12k of pet expenses and $8k of healthcare! Ouch. But that’s not really the case because monthly spikes happen and they aren’t consistent. Let’s look for January through June of 2021 to get a better idea.

When you look at 6 months of data the averages become more normal. We lost our dog to cancer in March so there were still a lot unusually high pet expense months but it’s $3k for the first half of the year. Barring anything catastrophic happening we’ll be able to keep things within the $3,500 pet expense budget for the year.

A similar story for healthcare. June was heavy but only $732 was spent from Jan-June or $106/mo.

Other Tools

I’m partial to YNAB because it’s just worked very well and I also use it for budgeting. But it does cost $84/year and while I think I more than save that much by using it in money and time that’s a turn off for some people.

Mint.com – Now owned by Intuit, the same company as TurboTax is a free tool for tracking expenses. It can also link to online accounts and import transactions. I tried it years ago and was frustrated in not getting my transactions and balances to match up. I know plenty of others that use it successfully though.

Spreadsheet – Old school but it works. It is a lot more work to do everything from manually entering transactions to summarizing the data but it is an option.

Paper – Even more old school with all the downsides of a spreadsheet plus you’ll have to manually calculate spending and averages.

There are a couple of side benefits worth noting by tracking spending in a detailed way.

More conscious spender – When you see real time how much money is going out the door it makes you more hyper aware of your spending. That in turn makes me think about purchases more carefully before I made them.

Awareness of fraud – By seeing every transaction that hits your accounts on a daily basis you will spot unusual transactions right away.

Easy to see all transactions – Instead of logging into each online account the data is all there right on one dashboard. I don’t have to go hunting down data figuring out which card and which month I spent something.

Peace of Mind – I’ve found that I have more peace of mind when I feel like I have the full spending picture.

Action Steps:

If you want to tiptoe in tracking spending:

Make a list of all your spending accounts and then look up what you spent last month using online summaries. How does that compare with what you thought? To your income?

Repeat that for the last 6 months. If you really want to dig in look up summary spending for the previous year.

If you want to jump all in:

Research the tracking tools like YNAB, Mint.com or others and pick one. I’m partial to YNAB which does have a free 35 day trial. If you use my referral link we each get a an extra free month of YNAB.

Make a list of categories to track. DON’T get paralyzed here! Take a stab at it thinking through your spending and run with it.

Track! Things will be slow at first with any tool but you’ll get faster and more efficient.

Don’t sweat the small stuff – some people obsess over where every penny goes. Don’t stress over every dollar. We’re looking to find and fix big spending issues, not little ones.

BLUF: Our experiences, like investments, have the ability to pay us a dividend long after the original experience is over in the form of happiness. These dividends increase our happiness through the recalling of those happy original experiences. Unlike investments, however, we have the ability to force those happiness dividends to be paid on demand through our actions.

Note: The cover photo is from the Albuquerque balloon festival, the largest in the world. The “balloon glow” is when all pilots stand up their balloons at night and illuminate them with the burner. It’s truly stunning to see and hear hundreds of balloons doing this at the same time.

I recently read the book Die with Zero by Bill Perkins. The title comes from the idea that to maximize your happiness in life you should really aim to spend down or give away all your money such that at the end you die with close to $0. A idea in that book that resonated with me was the concept that experiences, like money, can compound and pay dividends to us over the course of our life. The idea was especially intriguing to me since I’ve been changing my spending focus from things to experiences over the last 10 or so years.

My Journey Away From Consumerism

One very substantial change in my life that happened progressively over time was the change from valuing stuff to valuing experiences. I was very fortunate to grow up in an upper middle class family that could afford nice things. I got a TV for my room when I graduated elementary school. In the mid-90’s when computers were very expensive we constantly bought the latest trends whether it be a full desktop computer, a CD burning drive or having Road Runner high speed internet (cable modem).

As a twenty something I wanted to have all of the same cool new gadgets that seemed to be coming out constantly. When DVD players were brand new I was still in college making very little money and I bought one new for $500. I also put together a 5.1 surround sound system with the main driver being to watch this cool new movie that came out called “The Matrix.” As sweet as it was to hear bullets flying past your head for the first time, it was a lot of money to spend for a kid that didn’t really have any.

When my divorce happened at 31 and I was faced with both a tougher financial reality paying for a house and lifestyle alone along with going through the experience of separating “stuff.” I think that started to change my worldview that the pursuit of stuff wasn’t adding a lot to my life and it could of course disappear at any time. I also realized that the concerts, parties and vacations that I had experienced were a lot more enjoyable to me and started to focus a bit more on spending on my money there.

How Experiences Pay Us Back in Happiness Dividends

I used to think about stuff as more valuable than experiences because I perceived that stuff could keep paying me back with it’s utility. For example, that $500 DVD player is something that I could enjoy for at least two or three years watching movies. By contrast, if I took a $500 vacation for a long weekend then I thought that I would only get 3 days of enjoyment from that experience.

The experience itself was usually much cooler than the “thing” I would otherwise buy but the stuff had the capability to hang around in my life for much longer. To have more enjoyment from experiences meant that I would need to schedule another and another because the happiness derived from the experience only happened while I was living it.

Thinking about Individual Experiences

I could have a really great experience like a Caribbean cruise vacation one year and reap the benefits of that time away. Relaxing on the upper deck sipping a cocktail. Enjoying fancy restaurant meals or gut busting all you can eat buffets. Seeing great onboard entertainment like singers serenating us and comedians making us laugh until our stomach hurts. Taking excursions at port stops to have experiences like feeding the stingrays.

A great week that’s high up on the happiness scale but after a couple weeks back at work you’re thinking about what to do next. Then perhaps the next year you go see a great concert that you’ve always wanted to see. And then the next year you throw a surprise birthday party for a great friend of yours. Each event in itself is wonderful but they are each discreet events that when over, the happiness gained from that event effectively ends.

The Happiness Dividend Concept

This thinking was flawed though, because that’s not how experiences work when it comes to the happiness that we derive from them. There’s actually a cumulative effect to it where old experiences that are truly meaningful to you are stored in your memory banks. When you recall memories of that experience due to some trigger like looking at a picture, that experience pays you a happiness dividend. You are transported back to the time when the picture was taken and derive a sense of gratitude. If it was very memorable you might be able to recall the smell of the ocean from the cruse ship deck or the feel of the stingrays sucking food out of your hands.

Looking at my previous experience timeline example, the timeline actually starts to look at this. That Caribbean cruise was a tremendous experience in the year that it happened. However, in year two on the anniversary of the cruise your Facebook memories pop up with pictures from your cruise that happened one year ago and you are transported back. Maybe you sit down with your partner and open up the pictures from that trip and take a walk down memory lane. You laugh about the things that didn’t go right but turned out to be a great adventure. You enjoy recalling your favorite “remember when…” moments to each other.

The joy, gratitude and happiness that you feel during the recollection of fond memories is the happiness dividend being payed to you from that previous experience. You get paid this happiness dividend from that old experience and it didn’t cost you any money. Then the next year your friend comes to you thinking about taking a similar cruise and asks for your help in planning it since you’ve taken the cruise. You get to once again recall all of the details of the experience all while helping your friend. Another happiness dividend paid on the original experience.

Over time you see that this can cause your level of happiness to build from each successful new experience on top of the dividends paid from old experiences. Just like a financial dividend paid on a stock, the longer you have to remember the experience, the more time you have to be paid dividends. This is a strong motivating factor to really use the energy of your teens, 20’s and 30’s to make some great memories and get those happiness dividends flowing early in life. That maximizes the time in your life that you have for those experience based “investments” to pay you back in happy memories.

Being FI minded, there’s obviously a balance to find between spending all your money on experiences when you’re younger and have less income and saving and investing for the future. The great thing about being young, though, is that you’re typically willing to put up with some much cheaper and less comfortable options that the later in life you wouldn’t dream of doing. Backpacking around to travel, sleeping in hostels, taking long road trips, getting the cheap seats at a concert. The key thing is that you’re trying new things and making memories that you can then start recalling. No great story starts with “I went to bed early.”

Increasing Happiness Dividends

A beautiful thing about experience based happiness dividends is that you can control the size and frequency of that dividend. If only we had the ability to do that with our financial investments…

Increasing the Dividend Amount

Have you ever noticed that not all experiences are created equal? I’m not just talking about the “in the moment” how awesome it feels. I’m talking about how you feel years later when you think about memories of that experience. Why do you remember some more often than others? Why do you remember some very fondly and can be transported back to that place and time? Why are some barely able to be remembered?

To increase the dividend amount we want to have more fulfilling and impactful experiences. Unfortunately, I can’t give you a precise answer to that because it could be different for each of us. My opinion is that it can be one or more components that matter most to us.

Experience Components that May be Important:

Doing something new or novel. Often things I’m recalling are some experience that is very different from anything else in my life. For example, the article feature image are hot air balloons lighting up in the evening when the burners were turned.

It involves people. It could be family, friends or complete strangers. I’ve found that my richest experiences involve people. Often times it’s bonding with others using that experience. Sometimes the experience is really making a deep connection with another person through a meaningful, deep conversation.

It involves multiple senses – Touch, taste, sight, sound and smell.

It involves emotions. If you experienced excitement, anxiety, nervousness, joy, pain as a part of the experience it could very well become something that stands out in your memories.

It involves something that you already love as a hobby or passion. Animals, sports, race cars, painting or gardening just to name a few.

It involves laughter. There’s just something about laughter that not only makes you happy but can turn an average evening into a memorable one.

For me personally the one that seems to be most important is people. There’s something about experiences that involve connecting with people that make that one of the most important ingredients to my memorable experiences.

Increasing the Dividend Frequency

Forget quarterly dividends, when it comes to happiness dividends you actually have the ability to make them pay out on demand. The key is that you aren’t just leaving the recollection of those memories to chance due to a trigger from the environment around you like something on TV. If you take deliberate action then you can enable the recalling of memories when you want to.

One of my favorite ways is to post up pictures of my experience on social media like Facebook (FB) or Instagram (IG). On a daily basis I can pull up the “memories” and see everything that I experienced on that particular day. It transports me back in time reminding me of things that I had forgotten about. Vacations, festivals, concerts and any number of other memorable things. If I happen to be getting together with other people that were also part of that experience then the dividend can grow as we reminisce about that shared experience.

Ideas to Recall Memories more Consistently:

Post on social media and then look at FB memories, IG memories, FB/IG stories archive daily.

Post reviews of experiences on TripAdvisor.

Join travel groups and help share your knowledge which will also make you think back to those trips and look through pictures.

Make the recalling of memories a conversation topic when you get together with family and friends. Ask people to discuss their favorite experience from the past year.

Look at old photo albums / online archives from your experiences more regularly. Pick one or two and review it. I like to organize my photos chronologically by experience which makes this easier.

Do you have fond childhood memories of visiting a certain place or doing a certain activity? If you re-do that experience with other people that you care about like your children, other family or friends then you can create a whole new memory. However, that newer experience based memory has a connection back to the old memory because there’s a common thread of the experience. Now there’s a forever connection between the two and recalling either fond memory will pull forward the memory of the other.

For example, if going to the state fair and riding the Ferris wheel was a fond memory from your childhood then consider repeating that experience with your children and grand children. Repeating that experience will make you recall and tell stories about when you used to ride the Ferris wheel with your parents and how much you loved it. In the future you can then remember the experience both as a child and then as a parent sharing it with your child.

We Aren’t Getting any Younger

It’s also important to start young because some experiences will not be possible or desirable to do after a certain point. Despite what we may tell ourselves, our bodies age and get less capable over time. No matter how good the 50 year old you feels, your body can not handle and recover from physical activity like it could when 20. There are certain physical experiences that if you want to have them, you need to do them by a certain age.

Eventually they won’t be possible like climbing a high peak or taking an expedition to a remote jungle. Even if you are physically capable of doing it when older, it might be so much less enjoyable because of the increased aches and pains that you might not even want to do it. A hard truth is that one day you won’t be able to do most of these experiences. All that you will have will be your memories of past experiences to pay you happiness dividends. Start investing.

Action Steps:

Making Memorable Experiences:

Figure out what kinds of experiences bring you the most joy. Is it trying new things? Is it doing things with people? Combining experiences with things that you love? Figure out what you enjoy most and do more of that.

Consider bucketizing experiences by age range so that you do the most physically demanding ones earlier in life.

Make a plan to regularly research and seek out new experiences.

Try to make a backlog of things that you’d like to do and then actively work on planning to do each one.

Use some form of social media like FaceBook to document your experience.

Take lots of pictures but don’t miss the whole experience focused on capturing it with your phone.

Getting Happiness Dividends:

Look back at your Facebook memories on a daily basis. “On this day X years ago.” Don’t wait for the FB algorithm to maybe bring one up. Go to your profile > Memories section and look at all of them for that day.

Go through travel and experience pictures periodically.

Think back to a time or place in your life and try to recall every memory that you can. For example, every memory that you have from high school. Write them down as you go and see how much you can remember.

Join interest groups around your experiences like a Facebook travel group or forum so that you can recall and talk about those experiences.

Ask friends and family about their favorite experiences lately. In turn, share yours.

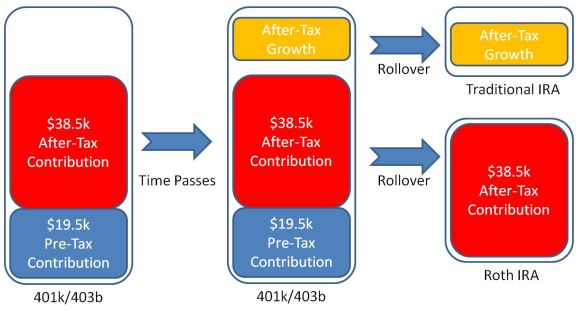

BLUF: A mega backdoor Roth rollover is a powerful way to get a boatload of money into a Roth account for those that have a 401k/403b/457 plan that allows it. You can go well beyond the $6k limit in 2021 up to as much as $38.5k extra a year.

Why I Wrote this Article